The Acquisition Exit Is Underrated and Most Founders Are Not Building for It

“In Silicon Valley, the most important thing to think about when starting a company is how you’re going to end it.”

– Mark A. Lemley & Andrew McCreary, Exit Strategy

The classic success story of startups has always been that they eventually go public. It is the ultimate endgame that most founders are told to build for. But look at how companies actually exit now, and you get a different story. Selling has become the path of least resistance, and acquisitions have become the new finish line.

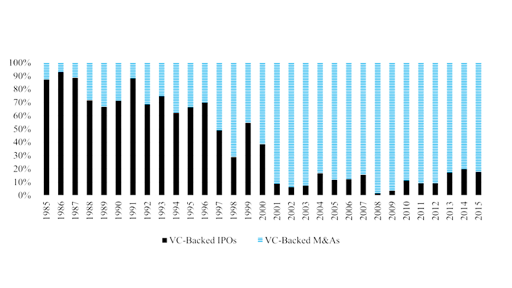

The exit picture has changed in just a generation’s time. IPOs have fallen from about 90% of exits a few decades ago to something approaching 10% today [1].

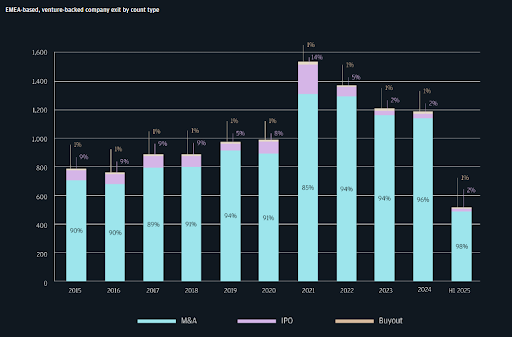

Research by J.P. Morgan shows that over the last five years, mergers and acquisitions accounted for more than 85% of venture-backed exits in Europe, the Middle East, and Africa, with the number of companies going public sitting at a decade low.

In the first quarter of 2026, acquisitions made up roughly 68% of US startup exits, according to PitchBook data, and the median M&A exit landed near $71 million. Over the same quarter, 15 venture-backed tech companies went public in the US, a pace of about 60 listings for the year. Thousands of companies were acquired.

Acquisitions now dominate how companies exit, yet selling still carries a stigma when, in reality, it deserves to be treated as a success story. To see why it counts as one, it helps to start with what an exit is actually for. To dispel this stigma, it makes sense to better understand and define the goals of an exit in the first place.

What Happened to IPOs?

Founders and their investors hold illiquid shares. At some point, they need to turn that paper into cash, and historically. Public markets were the most realistic route for that amount of liquidity.

This changed over the 2010s, as private equity investment ballooned. This meant that companies no longer had to go public to raise serious money. A decade of low interest rates sent institutions hunting for returns, and crossover funds like Tiger, sovereign wealth funds, SoftBank’s Vision Fund, and others started writing late-stage checks the size of small IPOs. Looser rules on staying private let companies take that money without being forced onto the public markets. So a company that needed a few hundred million could now raise it in a private round. For example, Databricks has raised well over 10 billion dollars this way while staying private for more than a decade. Companies now stay private far longer, and some raise more privately than they ever could have in an IPO.

The winner-take-all dynamics of the market left a small number of tech giants like Google, Meta and Amazon extraordinarily cash-rich, and gave them a strong motive to buy anything that might threaten or enable them. It’s the “Kronos effect” – as Tim Wu coined it – killing your competitors in their infancy. So for most startups, there is now almost always a credible buyer sitting out there somewhere.

The “sale” also happens to be the easier, faster deal. A VC fund has a roughly 10-year life-cycle and must return cash to its own investors. Acquisitions can close in a few months and pay out a predictable amount, while an IPO takes years of preparation, then leaves everyone holding volatile stock through a lockup. Given a choice between a quick, certain sale and a slow, uncertain listing, the incentive structure leans hard toward the sale.

Simply put, staying private and selling became so easy and so well funded that IPOs are just not that attractive anymore.

And yet somehow none of this has touched what founders are trained to want. The IPO is still the destination that gets glorified, yet few seem to reach it these days. Meanwhile, the acquisition, the thing that actually happens, still gets filed under a “compromise” that founders settle for.

How Acquisitions Got Misread

It’s not too surprising that the public adopted a negative view of acquisitions. For decades, researchers who study company exits treated firm exit as a single event that meant one thing, which was failure.

Back in the day, researchers worked from big registries that tracked active companies on a yearly basis, so when one dropped off the list, all they could see was that it was gone. There was no record of why it disappeared, but since companies usually vanish because they’ve failed, the update would signal a failure, such as a bankruptcy. And since companies usually vanish because they’ve failed, everything that left got filed as failure by default.

{Here’s a great site that shows startup use-cases and why they failed, just for fun}

Statistical offices only started recording the type of exit fairly recently, and at different times in different countries, with much of Europe reaching it in the late 2000s [1]. But once the records could tell the routes apart, the picture finally changed. However, the founder’s perception of the event is harder to change, which is why someone who sells still might feel like they lost.

Why Acquisitions Are Usually Better Than Founders Think

So a founder decides to sell. They get their cash, employees get the benefits, VCs get their return. But the value of selling goes beyond just turning private equity into cash.

The acquisition path should sit somewhere in every founder’s commercialization strategy from early on. Startups are great at discovering something valuable. With the right team, they can turn an idea into a real product and prove that customers want it. But scaling is a different challenge, and it can take years to build the machinery that gets a product from early traction to a much larger market. A good buyer can ensure that the finished product reaches customers on a far shorter timeline. And a not just good, but strategic buyer, will spend a lot of effort evaluating the company’s potential inside its own walls in order to turn it into something more valuable than it could ever have become alone. Selling can therefore unlock the company’s next stage of growth.

Of course, it is not easy for any founder to say goodbye to their “child.” They raise them from infancy, and how do they know the new parents will be right for it? So founders have to evaluate their buyers as closely as buyers evaluate them, and the emotional side is real, because you do not fully control what happens to the team and operations once the deal closes. Those are genuine costs that have serious weight.

But one thing founders rarely weigh seriously is a rational stopping point. Startup culture romanticizes persistence and the grind, yet you can grind a company into the ground and still not be doing what the business actually needs.

“We would all be better off if we did more quitting.”

– Steven Levitt

There is nothing noble about staying independent once the best risk-adjusted outcome is already sitting in your lap. A good sale lets a founder harvest the value they built, then carry that capital and energy into the next venture, or finally step back and enjoy a life that took years of work to earn. Either way, if you are a founder, this frees up your best resource, which is you.

Meanwhile, the acquisition can also reward the employees working for the startup. In many cases, startup employees take underpaid jobs for equity that is worth nothing until there’s a liquidity event, and they have far less control over whether that event ever comes.

A sale is often the only way that bet pays off for them. Declining a good acquisition because a founder personally wants to keep going is, in part, deciding on their behalf that they should keep waiting. And a company that stays independent and slowly fades takes everything down with it.

An acquisition can be how you pass the baton, so the thing you built keeps running instead of you.

Building For The Exit

So an acquisition can, in theory, create a lot of value. But what makes the difference between a good sale and a bad one, for the founder and the buyer alike?

The problem is that because most founders never plan for a sale, still thinking along the exit-equals-failure line, they never build the muscle that would make them acquirable in the first place.

Building for the potential acquisition needs to start early on, but preparing does not mean building a different company. Justin Kan, who wrote Y Combinator’s internal guide to selling a company, argues that the best way to build a company you could sell is almost identical to the way you build one that could stand on its own. I.e., create a strong product, real traction, clean operations, etc. But on top of all that, founders should build with the buyer’s logic in mind.

The best buyers keep an “always on” watch list, which includes what kinds of assets matter to their strategy. They continuously screen targets based on fit, integration risk, and value creation potential. A founder should reverse that by creating their own buyer map.

A thorough research campaign into their field should surface a list of potential acquirers, the companies with product gaps, missing tooling they would rather buy than build, and a habit of swallowing competitors. They should keep that list in view while steering the startup.

Sellers are almost always caught off guard by how much information a buyer demands, and the diligence materials need to be ready the day the LOI is signed. For a founder, that means the company has to be fully organized and clean, with the cap table in order, IP owned, and financials up to date. I.e., the paperwork should be organized and current at all times. This should be a given, yet it’s not always the case.

Secondly, preparing early lets founders build relationships with those acquirers, so that when the time comes, there is no scramble to fit into a buyer’s box, and no one ends up backed into the one-buyer corner. The best time to sell is always when the founder has options, and the sale is strongest when it is a choice.

Having options also screens out the wrong buyers. Dominant incumbents sometimes acquire startups to smother a threat, occasionally by shutting down the very thing they bought. A founder refusing a good deal does nothing to slow industry concentration that these acquisitions cause, that is the regulators’ job, but they can be deliberate about who they sell to. A sale to a generic dominant platform is not the same as a sale to a strategic peer or a company that genuinely needs the product to grow.

Building for the exit should mean building toward the good version of acquisition, because a good sale is rarely luck.

Two Companies, Two Endings

Take these two companies that both sold and landed in opposite places.

In April 2012, Instagram sold to Facebook for a billion dollars. It had 13 employees, no revenue, and around thirty million users. Three weeks before the deal, it had turned down a $525 million offer from Twitter, and it had just closed a round at a $500 million valuation that Zuckerberg then doubled. Instagram did not need to sell at the time, and that was its strength in negotiations. This is the reason it managed to get a billion dollars and also a promise to keep running independently. Its house was in order enough that the whole deal came together over a single weekend. Kevin Systrom walked away with roughly $400 million, the employees split about a hundred million, and the product continued to function inside its acquirer. It scaled into something with billions of users that no 13-person team could have built alone.

Now take Good Technology. A mobile security company, once valued at more than a billion dollars – a strong IPO candidate that filed to go public in early 2014. But then the listing stalled and never happened, and the company was burning cash and losing money on every dollar of revenue. The market further cooled on unprofitable tech, and the IPO it needed to raise money just never came, which left it with dwindling cash. This is the weakest position a company can negotiate from. In 2015, it sold to BlackBerry, a rival it had fought for years, for $425 million, less than half its private peak. The preferred stock held by the investors and executives was worth about three dollars a share, and the common stock held by the employees was worth 44 cents, roughly a tenth of what it had been the year before.

The moral of the story is that preparing for an exit should start at the beginning of a company. Had Good Technology treated an acquisition as a real path from the start, rather than betting everything on an IPO, it might have built the relationships and the leverage to sell from a stronger position instead of a fire sale to an old rival.

So the acquisition is worth taking seriously and worth preparing for, well before it is on the table. It is the most likely good outcome a startup gets, and it is not the failure it is often treated as. It can go well or badly, and the difference is mostly preparation. Build for it early, and you turn the likeliest ending into one you actually chose.

Continue the Conversation

Most of a company’s value is won or lost in the decisions that are easy to overlook. Arcanum Ventures pays attention to those early, working with founders and teams building in complex, high-stakes environments across emerging technologies.

We track these questions in public through podcasts, videos and original writing, while working directly with the people building inside them. Join us as a speaker, tune in, or keep pace with what’s moving across tech.

If you are building something difficult and want a second set of experienced eyes, we would love to hear from you.

References

[1] Cefis, E., Bettinelli, C., Coad, A. & Marsili, O. (2022). Understanding firm exit: a systematic literature review. Small Business Economics, 59(2), 423–446.

[2] Lemley, M. A. & McCreary, A. (2021). Exit Strategy. Boston University Law Review, 101, 1–101.

[3] Coleman, S., Cotei, C. & Farhat, J. B. (2010). Factors Affecting Survival, Closure and M&A Exit for Small Businesses. Midwest Finance Association 2012 Annual Meetings Paper.

[4] Sirower, M. L. & Weirens, J. M. (2022). The Synergy Solution: How Companies Win the Mergers & Acquisitions Game. Boston, MA: Harvard Business Review Press.

Emerging managers are often framed as “high-risk, high-reward,” but the data – and LP experience – tell a…

Traditional finance revolutionized asset access through mutual funds and ETFs. Today, tokenization is…

AI has expanded the scale of what gets collected about you far beyond what most people intuit. But each…